Contrary minded subscribers who have been tracking our forecast for the crude oil over the course of the last few months will appreciate this story about the “peaksters” and Wall Street’s conversion to a belief in $200/barrel crude oil. We’ll stand by the analysis presented in the August issue of The Elliott Wave Theorist, an excerpt of which is appears below. One of the more revealing statements in the article is contained in the phrase “As energy prices soar and violence convulses the Middle East.” Israel invaded Lebanon on July 12. Oil actually peaked July 14. So, for most of the time violence was convulsing the Mideast, oil was going down not up. It only seems like it’s been rising because the peak oil pronouncements have been as shrill as ever in the last few weeks. As they say on Wall Street: if it’s obvious, it’s obviously. Contrary minded subscribers who have been tracking our forecast for the crude oil over the course of the last few months will appreciate this story about the “peaksters” and Wall Street’s conversion to a belief in $200/barrel crude oil. We’ll stand by the analysis presented in the August issue of The Elliott Wave Theorist, an excerpt of which is appears below. One of the more revealing statements in the article is contained in the phrase “As energy prices soar and violence convulses the Middle East.” Israel invaded Lebanon on July 12. Oil actually peaked July 14. So, for most of the time violence was convulsing the Mideast, oil was going down not up. It only seems like it’s been rising because the peak oil pronouncements have been as shrill as ever in the last few weeks. As they say on Wall Street: if it’s obvious, it’s obviously.

The Elliott Wave Theorist

July 25, 2006

PEAK OIL” OR PEAK PRICE?

On March 16, 2006 I had the pleasure of speaking at the Kenos Circle Oil Seminar in Vienna, Austria. I made two major points: (1) The Elliott wave count for the advance in oil prices was not over yet, and (2) the psychology of the oil market was historically extreme. The only way to reconcile these two conditions was to recognize that the bulk of the bull market was over. Oil had already gone up seven times in value—a 600 percent gain—exhausting most of its profit potential. It would be lucky to gain one-tenth of that amount as it traced out its final two advancing waves.

The analysis presented then is still useful in today’s renewed environment of oil-price headlines and record oil futures trading volume.

Finished Goods, Financial Paper and Commodities

Finished goods are economic items. They move up and down primarily on the basis of their value to each potential customer relative to other values available. Stock and bond certificates are financial items created for speculative purposes. They move up and down primarily depending upon the mood of the herd that forms the market. Commodities are a hybrid of these two types of items. They have an economic component in their value to manufacturers who make finished goods, and they have a financial component in their value to investors who wish to speculate on the future course of prices.

The economic component of commodities is evident in the effect that their price fluctuations have on motivations within their related manufacturing industries. The financial component of commodities is evident in their occasional extreme values relative to other things. The recent run-up in copper is a case in point. Hedge fund managers engaged in herding to create one of the biggest speculative rises in copper ever, to the point that thieves have been gutting buildings to steal copper pipe and wire and sell it on the open market.

The price of oil reflects both its economic value—its use in fuel, plastics, etc.—and its financial value—its role as a vehicle for speculation. The more of the latter we find in a commodity, the more it tends to trace out Elliott waves.

How Market Psychology Works

Extreme opinions, shared widely, constitute the single most reliable indicator of an impending change of direction for a market. If virtually everyone is thinking one way, they have already acted, so the market has extremely limited potential to continue on its old path and huge potential to go the other way. This isn’t, but should be, taught in Finance 101. So-called “fundamentals,” contrary to common belief, are no help except in a contrary way when everyone cites them. News is useless except as an indicator of whether or not the market has reached this psychological condition.

[The dollar in late 2004 is] an example of extreme sentiment that we at EWI exploited to our advantage. News and opinion on the U.S. dollar in 2004 was as negative as we had seen on any market. The media relentlessly reported economists citing bearish “fundamentals.” (Almost no one was talking about bearish fundamentals at the peak in 2001.) By the end of 2004, the one-sided bearishness was so intense that we published a special section in The Elliott Wave Financial Forecast to express the tremendous potential for an upside reversal in the U.S. dollar. People thought we were crazy for being bullish. Yet, the dollar made its final bottom that month. A few months later, the sentiment had not abated, as indicated by a third magazine cover [in Newsweek]. In less than a year, the dollar index rose from 80.39 to 92.63, a 15 percent gain. Its latest retracement, to 83.60, by the way, has coincided with such negative psychology that the media are even listing the wealthy investors who are betting on further fall: Buffett, Gates, etc. The dollar, we conclude, is not finished rising, no matter what one claims about the “fundamentals.”

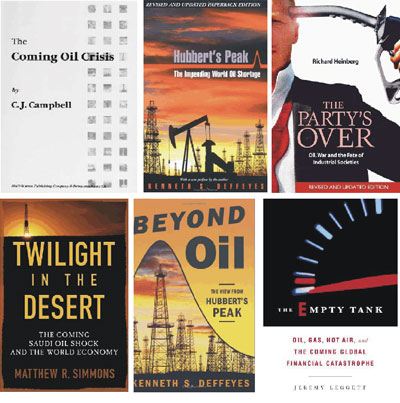

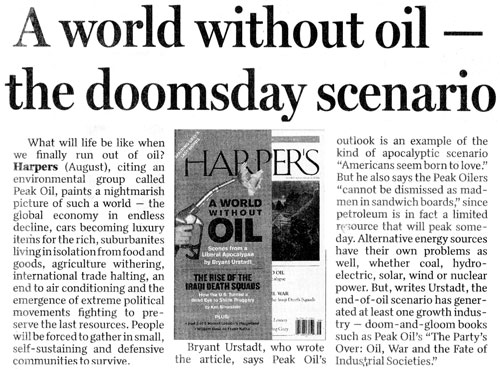

As I said in Vienna, the psychology in the oil market has been at least as one-sidedly positive as that for the dollar was one-sidedly negative, and probably more so. I have never, in 35 years of watching markets, seen such a consensus about any financial trend. The Internet is saturated with websites, media outlets, blogs, academics, economists and self-styled “Peak Oil” enthusiasts all calling for rising, if not infinitely rising, oil prices. And, by the way, there were no oil conferences when oil was selling for $10 a barrel.

These images show a smattering of the 16 books and countless headlines relating to oil that had been published in the months leading up to the temporary peak in crude oil prices on August 30, 2005. There are no balancing books because no one wrote any.

Speaking of the August 2005 high, The Elliott Wave Financial Forecast pointed out on September 2, 2005 that the 3-week average of the Bullish Consensus of financial professionals had reached a 10-year high in late August. On September 7, the Short Term Update reported that the Bullish Consensus survey now revealed “a whopping 96 percent bullish reading. Only 4% of those surveyed do NOT think that oil is going even higher from here.”

Almost immediately the energy sector rewarded the participants in this extremely one-sided market psychology by falling hard. Oil fell 21.8 percent, unleaded gas fell 42 percent and natural gas fell 59 percent respectively over the next several months. Heating oil also fell, despite the approach of winter. Today, after just an additional 10 percent gain, excitement is nearly as intense as it was at last year’s price peak.

As I further pointed out in the speech, the stock indexes for Abu Dhabi, Saudi Arabia and the financial stocks of Dubai had suddenly fallen 36%, 28% and 53% respectively. They have since fallen further. Because these indexes have turned weak, they must be skeptical of the miracle of ever-soaring oil prices.

|