Additional References

June 2004, EWFF

Add paintings to the list of “things” that have again become the object of investors’ affections. The art market just had its biggest month since May 1990. In addition to the all-time record price for a painting, $104.2 million for Picasso’s “Boy With a Pipe,” new records were set for works by a host of contemporary artists such as Jackson Pollack and 13 others. The obsession with paintings and other collectibles is an extension of the panic for stuff, which the April issue characterized as a curtain call for the mania’s post-peak echo. It is a twin to the high of May 1990, which was also accompanied by a spike in commodity prices and a brief burst in consumer prices. As disinflation re-asserted itself, however, a debacle referred to in art circles as the “nightmare of 1991” ensued. This time, the problem is not disinflation but outright deflation, so the coming downward pressure and collapse in art prices should be far deeper than in the early 1990s.

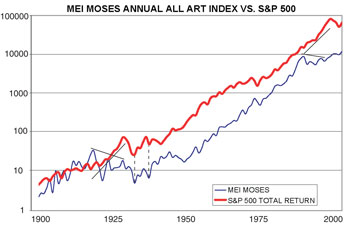

The art market’s rise in the wake of the 1987 stock market crash showed that art prices are not strictly commodities. Their price is also influenced by social mood as reflected by stock prices and regulated by the Wave Principle. Art prices appear to save their boldest moves for the aftermath of big advances, as well-heeled investors can afford to bid up “quality” works of art. The first great blow-out bid for a work of art, for instance, came right after the end of primary 3 in 1987, On November 11, 1987, Australian entrepreneur Alan Bond made his famous, and eventually ill-fated, purchase of Vincent Van Gogh’s “Irises.” In November 1989, just one month after a record high in the Value Line Arithematic Index, two more big-ticket paintings were sold. In May 1990, when the Dow Jones Composite, NASDAQ and Value Line had all recorded important peaks that would soon be confirmed by the Dow Industrials, the art market reached its great peak with the highest sales volume in history and a record price of $82.5 million for Van Gogh’s “Portrait of Dr. Gachet.” Here’s what The Elliott Wave Theorist said about the explosion as it was taking place:

What we are witnessing is one mania, an investment mania, with various outlets, art being one of them. What might surprise people is how closely the timing of their impulses and corrections is related. When the stock market finally tops out, art prices won’t be far behind.

The forecast was quickly followed by a washout for stocks (particularly in the Value Line and Dow Transport averages) that was even harder on buyers of art. Once again, the art market has carried to new heights in the wake of a Primary degree peak. A comparison to the peak of 1990 reveals many internal signals that the rally is on much weaker footing than its 1990 predecessor. For one thing, even though Picasso’s “Boy” finally broke the record set by Van Gogh’s “Dr. Gachet,” Artprice.com’s paintings index shows that the overall market for paintings is still below its level in 1990.

This inability of the art market to substantially surpass the old peak, despite ten years of bull market and a world awash in financial liquidity, suggests an extremely unstable uptrend. The death knell may have been a May 10 Barron’s article headlined, “Young Buyers are Plunging Into the Market.” It reveals that impressionists and old masters are being ignored for contemporary works that are “far more likely to double or triple in value in a short period.” This narrowing focus on objects of lesser quality is a dead ringer for the latter stages of the mania, when investors ignored stocks with long histories and established earnings records to flood into penny stocks with small floats and thus potential for a quick profit. Like investors who gave up on the Dow to ram the NASDAQ higher in February and March 2000, the new “collectors” have “little or no interest in works by what they call ‘dead artists.’” Descriptions of the atmosphere surrounding the “crazily hot” art scene are almost indistinguishable from those of the day-trading arena in 1999. “It’s about adrenaline,” says an art advisor. “It’s a fast-paced world, it’s exciting, it’s new. In a funny kind of way, collecting is the new cocaine.”

The focus of the rise is another important socionomic clue to the impending downswing. In May, abstract expressionism, the influential American art movement of the 1950s and 1960s bull market, topped the bill at the most prestigious contemporary art auctions. According to the Artlex Art Dictionary, the whole point of that era’s abstract expressionism was to “show feelings and emotions. It was generally believed that the spontaneity of the artists’ approach to their work would draw from and release the creativity of their unconscious minds.” The upward thrust of Cycle wave III, one of the most bullish periods of the entire Grand Supercycle advance, was so powerful that artists completely dispensed with any semblance of geometric form. Painting left the realm of the tangibly real and focused purely, and some experts say impeccably, on emotion. It makes perfect socionomic sense that, at the last stop for the euphoria of the Grand Supercycle peak, investors would reconnect with the emotion of Cycle III by bidding up the works that embody the energy and excitement of that quintessential bull market time.

It makes no financial sense, however, because the prevailing emotions, and thus tastes, are about to swing dramatically away from those that reigned through that time, so these high prices will not be maintained. The striking aspect of the Picasso that sold for $104 million is that it is so realistic. It is from 1905, two years before Picasso helped pave the way for abstract expressionism by founding the cubist movement. Ironically, in bringing such an extravagant price for a more traditional work, the market has managed to foreshadow, once again, the more prudent and conservative mood that is slowly working its way to the fore.

|